Buying a home is one of the biggest financial decisions most people will ever make. Between mortgage approvals, surveys, solicitor fees, and estate agent costs, the expenses stack up quickly. Yet one cost still catches buyers off guard more than almost any other: stamp duty. Despite being one of the highest upfront costs in any property purchase, stamp duty remains poorly understood by a significant portion of first-time buyers and even experienced movers. This guide breaks down everything you need to know about how stamp duty works in 2026, who pays it, how much it costs, and how to avoid any nasty surprises before you commit to a purchase.

What Is Stamp Duty and Why Does It Matter?

Stamp Duty Land Tax, commonly known as stamp duty, is a tax paid to HM Revenue and Customs when you buy a property or piece of land in England or Northern Ireland. Wales has its own version called Land Transaction Tax, and Scotland applies Land and Buildings Transaction Tax. The principle is the same across all three nations: when ownership of property changes hands above a certain value, the buyer owes a percentage of the purchase price to the government.

The tax is calculated in bands, much like income tax. You do not pay the same rate on the entire purchase price. Instead, different portions of the price fall into different bands, each with their own percentage. This tiered structure means that two buyers purchasing homes at similar prices can end up with noticeably different tax bills depending on their circumstances, whether they are first-time buyers, home movers, or investors purchasing additional properties.

For most buyers, stamp duty is due within 14 days of completing the purchase. Your solicitor or conveyancer handles the payment on your behalf, but the responsibility for ensuring it is paid correctly rests with the buyer. Getting this wrong can result in penalties, so understanding what you owe before you reach completion is essential.

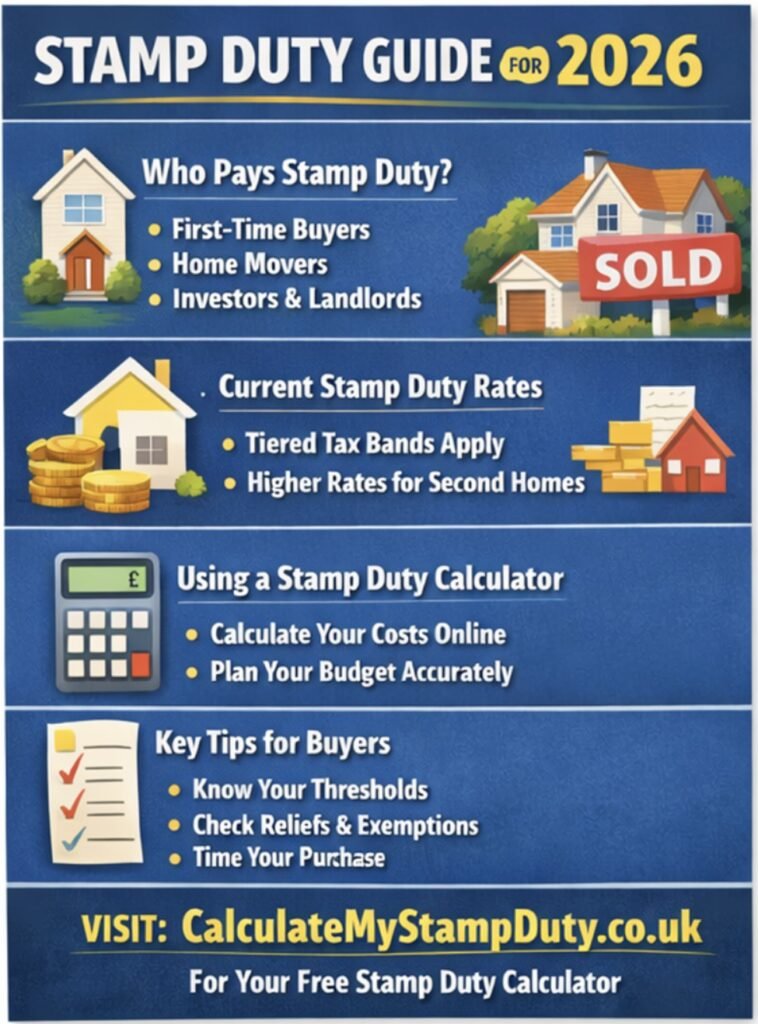

Who Pays Stamp Duty and Who Does Not?

Not every buyer pays stamp duty. Several reliefs and thresholds in place reduce or eliminate the bill for certain groups.

First-time buyers benefit from a dedicated relief that raises the threshold at which they start paying. This is designed to make it easier for people stepping onto the property ladder for the first time, recognising the particular financial challenge they face without the equity from a previous home to help fund their deposit.

Home movers pay stamp duty on a standard basis, which means the tax applies once the purchase price crosses the main residential threshold. The exact threshold has shifted in recent years following temporary reliefs introduced and then withdrawn, so it is worth confirming the current position before making any assumptions.

Landlords and second-home buyers face a surcharge on top of the standard rates. This additional rate applies to anyone who owns more than one residential property after completing their purchase. The surcharge has increased over time and represents a meaningful additional cost that property investors must factor into their returns.

Certain transactions are exempt entirely, including transfers between spouses or civil partners in certain circumstances, inherited properties, and some commercial arrangements. Your solicitor will advise on whether any exemption applies to your specific situation.

How the Rates Are Structured in 2026

The rates for 2026 follow a banded system that applies to different portions of the property’s value. To understand exactly how much you will owe, it helps to look at the current thresholds and percentages in detail. You can find a full breakdown of the 2026 Stamp Duty Rates on the Calculate My Stamp Duty website, which keeps its rate tables updated to reflect any changes made by the government.

The key thing to understand is that stamp duty is not a flat tax. If you buy a property for a price that falls into a higher band, you do not pay the higher rate on the entire sum. You only pay the higher rate on the portion of the price that sits within that band. The lower bands are charged at their respective rates as normal. This is a common misconception that leads many buyers to overestimate their bill, particularly those purchasing near the top of a given threshold.

For additional dwelling purchases, the surcharge is added on top of each band. So if the standard rate for a particular portion of the purchase price is three percent, a second-home buyer would pay that rate plus the surcharge on the same slice. The total can become substantial on higher-value properties, which is why investors increasingly factor stamp duty into their acquisition costs before making an offer.

Using an Online Calculator to Avoid Surprises

Given the complexity of stamp duty calculations, trying to work out your bill manually introduces room for error. The banded structure, the different rules for first-time buyers, the additional dwelling surcharge, and the varying thresholds across different buyer types all interact in ways that make a simple multiplication approach unreliable.

The most practical solution is to use a dedicated stamp duty calculator before you get too far into any property search. A reliable calculator takes into account your specific circumstances, the purchase price, whether you are a first-time buyer, and whether you will own multiple properties after completion. It then applies the correct rates to the correct portions of the price and presents your total liability in a clear, easy-to-read format.

https://calculatemystampduty.co.uk/ is the direct link to the free calculator tool available on Calculate My Stamp Duty. The tool is straightforward to use and produces an instant result, which makes it useful both early in your property search when you are budgeting in broad terms and later when you are comparing specific properties.

Running the numbers before you make an offer is genuinely valuable. It allows you to assess whether a property is within your budget once all costs are accounted for, and it can inform your negotiation strategy. In some cases, buyers have been able to negotiate a small reduction in the asking price to offset their stamp duty liability, particularly in slower markets where sellers are motivated.

Planning Around Stamp Duty: Practical Tips for 2026 Buyers

There are several practical steps buyers can take to manage their stamp duty liability effectively.

The first is to run your calculations early. Many buyers only think about stamp duty once they have found a property they want to buy, at which point they are already emotionally invested. Knowing your potential liability from the start of your search means you can set a realistic budget that accounts for all costs, not just the deposit and mortgage repayments.

The second is to understand the first-time buyer relief fully before assuming you qualify. The relief applies to the main residence you are purchasing, and there are rules around what counts as a first-time buyer that can catch some people out. If you have ever owned a property anywhere in the world, including inherited property in some circumstances, you may not qualify. Your solicitor will confirm your eligibility, but it is worth researching the rules yourself beforehand.

The third tip is to consider the timing of your purchase if you are moving between properties. There is a period during which you can own two properties simultaneously while the purchase of your new home is being completed and the sale of your old home has yet to go through. In this window, the additional dwelling surcharge may technically apply. However, there is a refund mechanism available if you sell your previous main residence within a set period. Understanding this process ahead of time prevents an unexpected tax bill from derailing your plans.

For landlords and investors building a portfolio, stamp duty planning has become a significant part of the acquisition strategy. Some investors time their purchases to take advantage of any temporary reliefs, while others factor the surcharge directly into their yield calculations and only proceed when the numbers still stack up.

Additional Tools and Resources Worth Exploring

Beyond the core stamp duty calculator, there is a range of additional tools that property buyers and investors find useful when planning a purchase. From affordability calculators to Land Registry data tools, having access to the right resources at the right time can make the whole process feel more manageable. You can explore a broader selection of property finance tools at https://calculatemystampduty.co.uk/tools, which brings together several useful calculators in one place.

These tools are particularly helpful for buyers who are comparing multiple properties at once or who want to model different scenarios before committing to a decision. Running the stamp duty calculation on three or four shortlisted properties, for example, can reveal meaningful differences in upfront costs that might influence which one you pursue.

Keeping Up With Rule Changes

Stamp duty rules do not stay fixed for long. The government has adjusted thresholds, introduced and removed temporary reliefs, and changed the surcharge on additional dwellings several times over the past decade. The period following a Budget announcement, in particular, often brings changes that affect buyers in the months ahead.

The most reliable way to stay informed is to consult up-to-date resources rather than relying on information that may have been accurate a year or two ago but no longer reflects current rules. Rate pages and calculators that are actively maintained provide the best protection against acting on outdated figures. Given how much money is at stake in any property transaction, a few minutes spent verifying your understanding of the current rules is always time well spent.

Whether you are buying your first home, moving up the ladder, or expanding a property portfolio, getting your stamp duty calculation right is a non-negotiable part of the planning process. The tools and rate information available at Calculate My Stamp Duty make that task straightforward, so there is no reason to head into any purchase without a clear picture of what you owe.