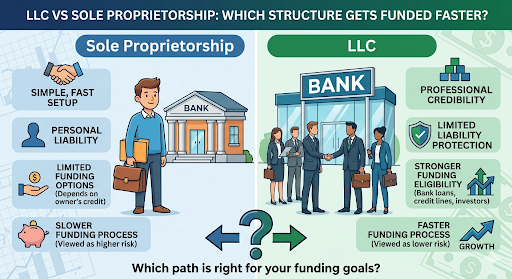

Choosing the right business structure isn’t just about taxes or paperwork—it directly impacts how quickly you can access funding. Whether you’re applying for a bank loan, business credit line, or investor capital, lenders evaluate risk first. And your business structure plays a major role in that decision.

Requirements for Modern Business Credit Lines

To qualify for business funding today, lenders expect more than just a good idea. They require a structured, verifiable, and compliant business entity.

Key requirements include the following:

- Registered business with the Secretary of State (SOS)

- Employer Identification Number (EIN)

- Business bank account (separate from personal)

- Professional business address and phone number

- Established business credit profile (DUNS, Experian, Equifax)

- Legal documents (licenses, operating agreements, etc.)

Comparison Table: Basic Credit Requirements

| Requirement | Sole Proprietorship | LLC |

| SOS Registration | Not Required | Required |

| EIN (Optional vs Required) | Optional | Required |

| Separate Business Identity | No | Yes |

| Business Credit Eligibility | Limited | Strong |

| Legal Documentation | Minimal | Structured |

The Role of the Secretary of State (SOS) Registration

SOS registration is often the first credibility checkpoint for lenders. When your business is officially registered:

- It becomes searchable in public records

- It proves your business is legitimate and active

- It creates a legal separation between you and your business

Without SOS registration, sole proprietors are often viewed as informal or high-risk borrowers.

Why Banks Demand Formal Operating Agreements

An Operating Agreement is more than a formality—it’s a risk management document for lenders.

Banks require it because it:

- Defines ownership structure

- Clarifies decision-making authority

- Shows long-term business planning

- Reduces internal disputes risk

Sole proprietors lack this structure, which can slow or even block funding approvals.

The Underwriter’s Perspective: Why Banks Rate LLCs as “Low Risk”

From a lender’s viewpoint, an LLC provides predictability, transparency, and accountability—all critical for risk evaluation.

Why LLCs Stand Out:

- Clear legal identity separate from the owner

- Easier to track financial history

- More stable operational structure

- Higher compliance with regulations

Risk Assessment Models for Registered Entities vs. Individuals

Banks use scoring models to evaluate risk. These models favor entities with documented histories.

How Risk is Evaluated:

- Credit history (business vs personal)

- Revenue consistency

- Legal structure stability

- Compliance records

Risk Comparison Table

| Factor | Sole Proprietor | LLC |

| Risk Level | High | Low to Medium |

| Credit Evaluation | Personal Only | Business + Personal |

| Transparency | Low | High |

| Default Risk Perception | Higher | Lower |

The Advantage of Verifiable Business Longevity

Lenders prioritize businesses with a clear separation of identity. You can learn more about how these formal structures impact your eligibility in our [guide to business structure differences].”

LLCs offer:

- Registered formation date

- Annual filings and compliance records

- Public verification of existence

Sole proprietorships lack:

- Verifiable timeline

- Documented continuity

- Transferable business identity

This makes LLCs appear more stable and fundable over time.

Building a Strong Financial Profile for Your Startup

Regardless of structure, building a solid financial foundation is essential—but LLCs have a clear advantage.

Steps to Strengthen Your Profile:

- Open a dedicated business bank account

- Maintain clean financial records

- Register with credit bureaus

- Pay vendors on time

- Keep liabilities separate from personal finances

Navigating Small Business Administration (SBA) Loan Requirements

SBA loans are among the most popular funding options—but they come with strict requirements.

SBA Expectations:

- Registered business entity (LLC preferred)

- EIN and business bank account

- Business plan and financial projections

- Proof of revenue or operational history

- Good credit (personal + business)

SBA Eligibility Comparison

| Criteria | Sole Proprietor | LLC |

| Eligibility | Limited | Strong |

| Documentation Strength | Low | High |

| Approval Speed | Slower | Faster |

| Funding Amount Potential | Lower | Higher |

How to Build Corporate Credit Without Using Your Social Security Number

One of the biggest advantages of an LLC is the ability to build credit separate from your personal identity.

Steps to Build Business Credit:

- Obtain an EIN (instead of SSN)

- Register for a DUNS number

- Open a business credit card in the company name

- Work with vendors that report to credit bureaus

- Pay all obligations on time

Benefits:

- Protects personal credit score

- Increases borrowing capacity

- Builds long-term financial independence

Conclusion

When it comes to securing funding quickly, an LLC clearly outperforms a sole proprietorship. Lenders prioritize businesses that are structured, transparent, and verifiable—and LLCs check all those boxes.

While sole proprietorships are easy to start, they often struggle to meet modern lending standards. An LLC not only improves your chances of approval but also speeds up the funding process by reducing perceived risk.

If your goal is fast, scalable access to capital, forming an LLC isn’t just an option—it’s a strategic advantage.

Business Funding FAQs

Q: Can a Sole Proprietor get a business loan?

Yes, but it’s usually harder. Lenders rely on your personal credit and income, which may limit approval chances and funding amounts compared to an LLC.

Q: Why do banks ask for my LLC formation documents?

Banks need proof that your business is legally registered and separate from you. These documents verify legitimacy, ownership, and reduce lending risk.

Q: Does BusinessRocket provide the documents needed for a bank account?

Yes, BusinessRocket typically provides essential formation documents like Articles of Organization and EIN assistance, which banks require to open a business account.